Guide to Blockchain Technology: Everything You Need to Know

Blockchain technology has emerged as one of the most revolutionary innovations of the 21st century, reshaping industries such as finance, healthcare, supply chain, and many others. While its roots lie in the world of cryptocurrencies, blockchain has evolved into a powerful technology with applications far beyond digital currencies. In this guide, we will dive deep into blockchain technology, explaining its principles, features, applications, and future prospects. This in-depth exploration aims to provide an all-encompassing understanding of blockchain, catering to both beginners and professionals.

Contents

What is Blockchain?

Blockchain is a decentralized and distributed ledger technology that allows data to be stored across a network of computers in a way that ensures security, transparency, and immutability. In essence, it is a chain of blocks, where each block contains a record of transactions, a timestamp, and a cryptographic hash linking it to the previous block. This design ensures that the data is tamper-proof and highly secure.

At its core, blockchain eliminates the need for intermediaries by enabling peer-to-peer transactions. By decentralizing control, blockchain promotes transparency and accountability, making it a groundbreaking solution for numerous challenges in traditional systems. The concept of blockchain was first introduced in 2008 by an anonymous entity known as Satoshi Nakamoto in the context of Bitcoin, the first cryptocurrency. Since then, blockchain has grown into a standalone technology with a wide array of applications.

Key Features of Blockchain

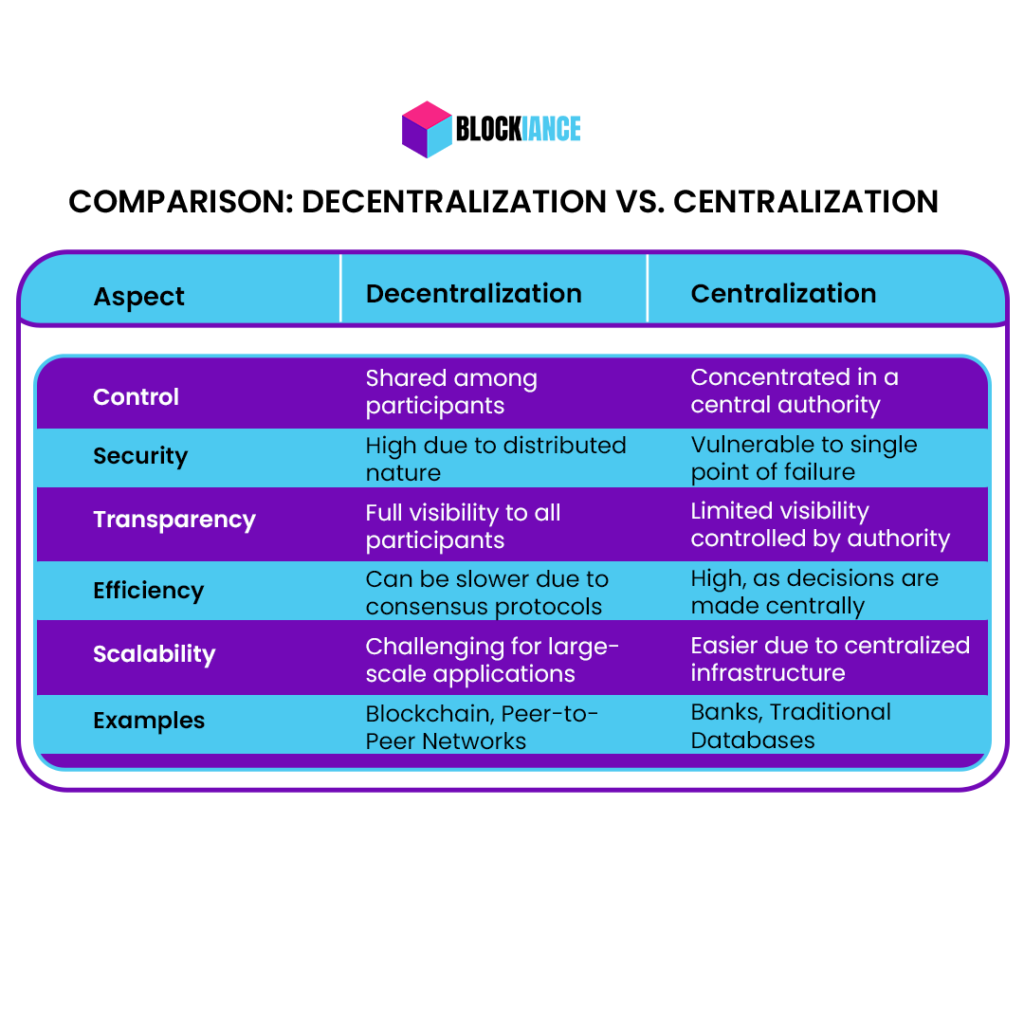

Decentralization

Decentralization is one of the most critical aspects of blockchain. Unlike traditional systems where a central authority manages data, blockchain distributes data across multiple nodes (computers) in the network. This distribution eliminates single points of failure and enhances system resilience. Each node in the network has a copy of the entire blockchain, ensuring that no single entity can control or manipulate the data.

Transparency

Transparency is another hallmark of blockchain technology. In public blockchains, such as Bitcoin and Ethereum, all transactions are visible to participants. This level of transparency fosters trust among users and ensures accountability. For example, in a financial context, blockchain enables anyone to verify transactions without relying on intermediaries like banks.

Immutability

Immutability refers to the inability to alter or delete data once it has been recorded on the blockchain. This is achieved through cryptographic hashing and consensus mechanisms. When a transaction is added to a block, it becomes permanently embedded in the blockchain’s history, making it resistant to tampering and fraud.

Security

Blockchain employs advanced cryptographic techniques to secure data and transactions. Each block is linked to the previous block using a unique cryptographic hash, creating a chain that is nearly impossible to alter. Additionally, the decentralized nature of blockchain makes it highly resistant to hacking attempts, as compromising one node does not affect the entire network.

Consensus Mechanisms

Consensus mechanisms ensure that all nodes in the network agree on the validity of transactions before adding them to the blockchain. Common consensus algorithms include Proof of Work (PoW), Proof of Stake (PoS), Delegated Proof of Stake (DPoS), and Byzantine Fault Tolerance (BFT). These mechanisms prevent malicious actors from manipulating the network.

How Blockchain Works

Blockchain technology operates through a series of well-defined steps:

Step 1: Transaction Initiation

A user initiates a transaction by sending data (e.g., transferring cryptocurrency) to the blockchain network. This data is digitally signed using the user’s private key to ensure authenticity.

Step 2: Transaction Broadcast

The transaction is broadcast to a network of nodes for validation. Each node independently verifies the transaction’s validity based on predefined rules, such as checking the sender’s account balance.

Step 3: Block Creation

Once validated, the transaction is grouped with other validated transactions to form a block. Each block contains a unique cryptographic hash, a timestamp, and the hash of the previous block, ensuring continuity.

Step 4: Consensus

The network’s nodes use a consensus mechanism to agree on the validity of the new block. For example, in Proof of Work (PoW), nodes (miners) solve complex mathematical puzzles to validate blocks.

Step 5: Block Addition

The validated block is added to the blockchain, linking it to the previous block. This linkage creates an immutable chain of blocks, ensuring the integrity of the data.

Step 6: Distribution

The updated blockchain is distributed across all nodes in the network. Each node updates its copy of the blockchain, ensuring consistency and synchronization.

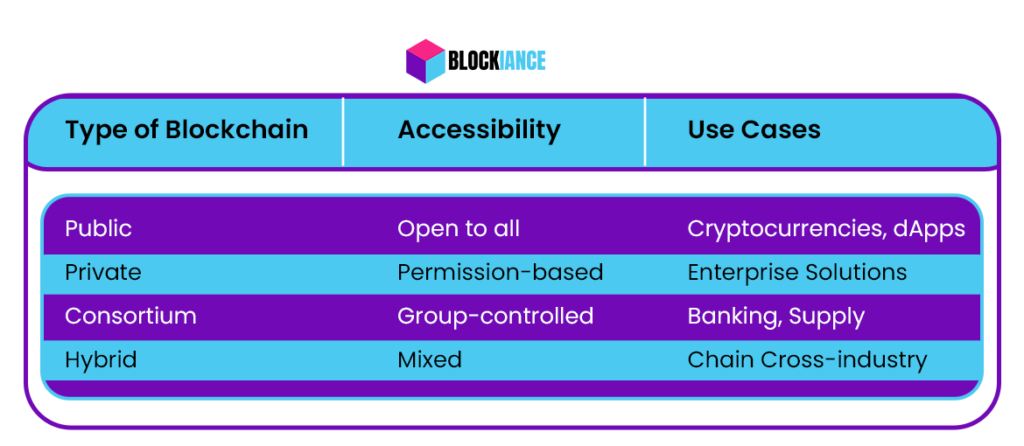

Types of Blockchains

Blockchain technology comes in various forms, each suited for specific use cases. The four main types of blockchains are:

Public Blockchain

A public blockchain is open to anyone who wishes to participate. These blockchains are fully decentralized and operate on a peer-to-peer network. Examples include Bitcoin and Ethereum. Public blockchains are ideal for applications requiring transparency and trust, such as cryptocurrencies.

Private Blockchain

A private blockchain is restricted to a specific organization or group of organizations. Access is limited, and only authorized participants can validate transactions. Private blockchains offer greater control and are often used in enterprise settings for applications like supply chain management and internal data sharing.

Consortium Blockchain

A consortium blockchain is controlled by a group of organizations rather than a single entity. It is partially decentralized and provides a balance between transparency and control. This type of blockchain is often used in industries like banking, where multiple entities collaborate.

Hybrid Blockchain

Hybrid blockchains combine elements of both public and private blockchains. They allow organizations to control certain aspects of the network while maintaining transparency for specific data. Hybrid blockchains are used in applications that require both privacy and public verification.

Applications of Blockchain

Blockchain technology is versatile and has a wide range of applications across various sectors. Here are some of the most prominent use cases:

Cryptocurrencies

Blockchain’s most well-known application is in cryptocurrencies such as Bitcoin, Ethereum, and Litecoin. These digital currencies operate on decentralized blockchain networks, enabling secure and transparent financial transactions without intermediaries.

Supply Chain Management

Blockchain enhances supply chain transparency by providing a tamper-proof record of goods as they move through the supply chain. Companies can track the origin, transit, and destination of products, reducing fraud and ensuring authenticity. For example, Walmart uses blockchain to track food products for safety and quality.

Healthcare

In the healthcare sector, blockchain can securely store and share patient records, ensuring data privacy and reducing administrative costs. Smart contracts can also be used to automate insurance claims processing and medication tracking.

Smart Contracts

Smart contracts are self-executing agreements with predefined terms written into code. These contracts automatically execute actions when conditions are met, eliminating the need for intermediaries. For instance, smart contracts can automate real estate transactions, reducing delays and costs.

Voting Systems

Blockchain-based voting systems ensure transparency and prevent election fraud. Each vote is recorded as a transaction on the blockchain, providing an immutable and verifiable record. This technology has the potential to revolutionize democratic processes by increasing voter confidence.

Decentralized Finance (DeFi)

Decentralized Finance (DeFi) leverages blockchain to offer financial services like lending, borrowing, and trading without traditional banks. Platforms like Uniswap and Aave enable users to trade cryptocurrencies and earn interest on their holdings.

Real Estate

Blockchain simplifies real estate transactions by enabling tokenized ownership. Property ownership records can be stored on the blockchain, reducing paperwork and increasing transparency.

Identity Management

Blockchain enables secure and tamper-proof identity verification. Digital identities stored on the blockchain allow individuals to control access to their personal data, reducing identity theft risks.

Intellectual Property Rights

Creators can use blockchain to protect intellectual property rights by creating immutable records of ownership. Artists, writers, and musicians can tokenize their works and sell them directly to consumers, bypassing intermediaries.

Challenges in Blockchain Adoption

Despite its immense potential, blockchain technology faces several challenges that need to be addressed for widespread adoption:

Scalability

Scalability remains a significant issue for blockchain networks. Public blockchains like Bitcoin and Ethereum often experience slow transaction speeds and high fees during periods of high demand. Solutions such as sharding and layer-2 scaling aim to address these challenges.

Regulatory Uncertainty

Blockchain operates in a legal gray area in many countries. Governments are still grappling with how to regulate cryptocurrencies and blockchain-based businesses. This uncertainty can deter organizations from adopting blockchain technology.

Energy Consumption

Proof of Work (PoW) consensus mechanisms, used by Bitcoin, consume vast amounts of energy. This environmental concern has led to the development of more energy-efficient mechanisms like Proof of Stake (PoS).

Interoperability

Different blockchain platforms often operate in isolation, limiting their ability to communicate and share data. Projects like Polkadot and Cosmos aim to bridge this gap by enabling cross-chain communication.

Complexity

Implementing blockchain solutions can be technically complex and resource-intensive. Businesses need skilled developers and substantial investments to design, deploy, and maintain blockchain-based systems. The lack of standardization across platforms often adds to the challenge, as organizations must customize solutions to meet their unique needs.

Additionally, integrating blockchain with existing systems can disrupt workflows and require extensive testing to ensure compatibility and security. Overcoming these complexities demands a well-thought-out strategy, collaboration with blockchain experts, and a focus on scalability and user-friendly interfaces to facilitate adoption.

Integration Challenges

Businesses looking to integrate blockchain must overcome technical hurdles such as adapting legacy systems to work with blockchain. The lack of standardized frameworks and tools can make integration costly and time-consuming.

Public Perception and Trust

Although blockchain is widely regarded as secure and innovative, there is still a lack of trust and understanding among the general public. Education and awareness campaigns are essential to demystify the technology and encourage its adoption.

Security Threats

While blockchain is inherently secure, vulnerabilities in applications built on blockchain (like wallets and smart contracts) can expose users to risks. Ensuring the robustness of these layers is vital to prevent cyberattacks and financial loss.

Future of Blockchain Technology

The future of blockchain technology is incredibly promising. Innovations in the field are set to overcome current limitations and unlock new possibilities. Key trends shaping the future of blockchain include:

Adoption of Blockchain 3.0

Blockchain 3.0 focuses on scalability, sustainability, and interoperability. It builds on earlier generations to address inefficiencies and expand the scope of blockchain applications.

Integration with Emerging Technologies

The convergence of blockchain with technologies like artificial intelligence (AI), the Internet of Things (IoT), and 5G will create transformative applications. For instance, IoT devices powered by blockchain can enable secure machine-to-machine communication.

Government and Enterprise Use Cases

Governments and enterprises are exploring blockchain for identity verification, land registry systems, tax collection, and digital currencies. Central Bank Digital Currencies (CBDCs) are a prime example of how blockchain could revolutionize the global financial system.

Evolution of Smart Contracts

Smart contracts are evolving to handle more complex and conditional transactions, enabling advanced use cases in sectors like insurance, healthcare, and real estate.

Green Blockchain Solutions

With concerns about energy consumption, the adoption of energy-efficient consensus mechanisms like Proof of Stake and the development of carbon-neutral blockchains will likely become a priority.

Conclusion

Blockchain technology represents a paradigm shift in how we store, share, and verify information. From its origins as the foundation for cryptocurrencies to its current role in reshaping industries, blockchain has proven to be a versatile and transformative innovation. As technology evolves, it will undoubtedly unlock new opportunities and applications, addressing the challenges that currently hinder its widespread adoption.

Understanding blockchain’s principles, features, and applications is essential for individuals and organizations looking to stay ahead in an increasingly digital and decentralized world. The journey of blockchain has just begun, and its potential is limited only by our imagination and willingness to innovate.

Amelia is a senior writer at Blockiance, focusing on the cultural implications of NFTs and digital ownership. Holding a master’s in media studies, she combines her academic background with a passion for storytelling to explore how Web3 technologies reshape creative industries.